Corporate Real Estate Valuation Services: Methodologies, Applications, and Strategic Implications

Corporate real estate represents a critical component of organizational capital, often constituting a significant portion of balance sheets for multinational corporations, institutional investors, and large enterprises. Accurate, independent, and standards-compliant valuation of these assets is essential for financial reporting, risk management, investment decisions, and strategic portfolio planning. This article examines corporate real estate valuation services, exploring methodologies such as income capitalization, discounted cash flow (DCF), cost approach, and sales comparison, with technical detail on their application and limitations. Regulatory compliance with IFRS, IVS, and local statutory frameworks is discussed, alongside emerging challenges, including ESG integration, market volatility, and technological disruption. Case illustrations and scenario analyses highlight practical applications, emphasizing the strategic importance of rigorous valuation in corporate governance and decision-making.

1. Introduction

Real estate assets in corporate portfolios are among the most strategically and financially significant investments. Offices, industrial warehouses, retail centers, hospitality properties, and specialized institutional buildings frequently represent billions of dollars in asset value. Consequently, corporate entities require valuation services that provide transparent, reliable, and defensible assessments.

Valuation underpins multiple organizational imperatives:

-

Financial Reporting: Aligning property values with IFRS or GAAP standards for fair presentation in audited financial statements.

-

Investment Strategy: Informing acquisition, disposal, or development decisions.

-

Risk Management: Assessing exposure, insurance adequacy, and portfolio vulnerability.

-

Regulatory Compliance: Ensuring adherence to statutory requirements and corporate governance frameworks.

Unlike residential or single-asset appraisals, corporate real estate valuation integrates complex lease structures, portfolio interdependencies, and strategic asset objectives. This research paper explores the theoretical and practical aspects of corporate real estate valuation, with an emphasis on methodologies, applications, standards, and emerging trends.

2. Literature Review and Theoretical Framework

The valuation of corporate real estate is informed by both economic theory and professional standards. The foundational premise is that property value reflects anticipated economic benefits, adjusted for risk, utility, and market constraints (RICS, 2022; IVSC, 2023).

2.1 The Role of Valuation in Corporate Governance

Corporate real estate valuation contributes to:

-

Strategic alignment: Matching asset utilization with business objectives.

-

Financial transparency: Providing defensible, audit-ready assessments.

-

Risk mitigation: Quantifying exposure to market volatility, vacancy, and obsolescence.

Studies indicate that robust valuation practices improve capital allocation efficiency and reduce systemic risk in corporate portfolios (Fanning, 2021; Geltner et al., 2014).

2.2 Valuation Standards

Professional valuation standards ensure consistency, reliability, and transparency:

-

International Valuation Standards (IVS) provide globally recognized definitions, methodologies, and reporting protocols.

-

RICS Red Book stipulates guidance for compliance, professional ethics, and documentation.

-

IFRS and GAAP frameworks specify fair value measurement requirements, particularly IAS 16 and IAS 40, critical for corporate reporting.

Integration of these standards supports defensible valuations, essential for financial audits, lending, and transaction due diligence.

3. Basis of Value in Corporate Real Estate

Corporate valuation relies on clearly defined bases of value, each suited to specific applications.

| Basis of Value | Definition | Primary Use |

|---|---|---|

| Market Value | Price obtainable in a competitive market between willing buyer and seller | Transactions, financial reporting |

| Fair Value | IFRS-defined price received in orderly sale, reflecting market participant assumptions | Financial statements, IFRS compliance |

| Investment Value | Value to a specific investor, considering financing, strategy, and objectives | Internal investment decisions, portfolio planning |

| Special Purpose / Forced Sale | Value in constrained or distressed sales | Insolvency, liquidation, accelerated divestments |

Selection of the appropriate basis is critical, as it influences the outcome, strategic interpretation, and compliance with regulatory and accounting frameworks.

4. Methodologies in Corporate Valuation

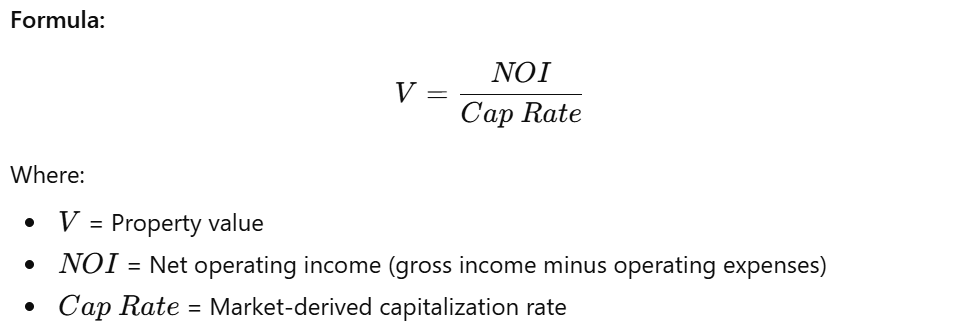

4.1 Income Capitalization Approach

The income capitalization method converts expected property income into present value using capitalization rates.

Application: Income-producing office buildings, retail centers, and industrial assets.

Adjustments: Vacancy allowance, rent-free periods, lease escalations, and operational expenses.

Limitations: Relies heavily on market-derived cap rates, which may fluctuate with interest rates and investor sentiment.

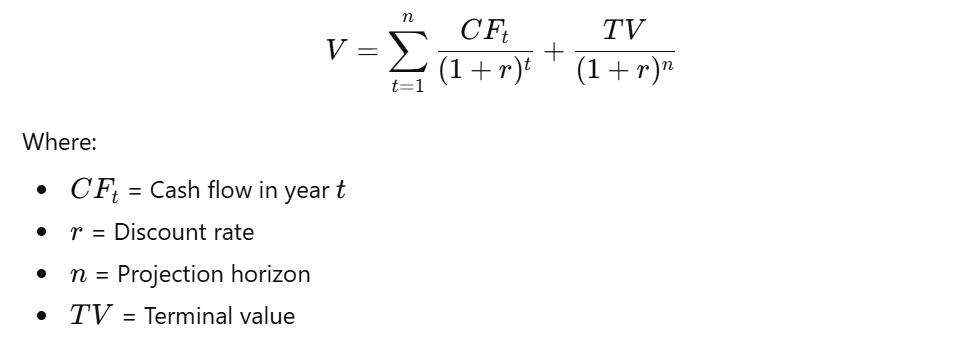

4.2 Discounted Cash Flow (DCF) Analysis

DCF evaluates the present value of projected cash flows, incorporating risk adjustments.

Formula:

Application: Development projects, complex portfolios, and properties with variable income streams.

Strengths: Accounts for timing of cash flows, capital expenditure, and growth assumptions.

Challenges: Requires accurate projections and sensitivity analysis for assumptions.

4.3 Cost Approach

The cost approach estimates value based on reproduction or replacement cost minus depreciation.

Application: Specialized or owner-occupied properties, institutional assets with limited market comparables.

Limitations: May not reflect market conditions; often used as a corroborative method.

4.4 Sales Comparison Approach

The sales comparison method benchmarks against recent market transactions, adjusting for differences in:

-

Size, location, and condition

-

Age and quality of construction

-

Lease structure and occupancy

-

Market liquidity and buyer demand

Application: Land, commercial office properties, and retail assets with sufficient comparable transactions.

Limitations: Data availability is critical; less applicable in opaque or thin markets.

5. Corporate Valuation Across Property Types

5.1 Office and Commercial Assets

Valuation considers:

-

Tenant quality and creditworthiness

-

Lease duration and escalation clauses

-

Building specification and grade

-

Location and accessibility

5.2 Industrial and Logistics Facilities

Valuation focuses on:

-

Functional utility (ceiling height, floor load, access)

-

Proximity to transportation networks

-

Lease terms and tenant stability

-

Potential for expansion or redevelopment

5.3 Retail and Mixed-Use Developments

Valuation includes:

-

Tenant mix and turnover-linked leases

-

Footfall and consumer trends

-

Anchor tenant influence

-

Integrated assessment across residential, commercial, and leisure components

5.4 Specialized Institutional Properties

Valuation requires:

-

Operational and functional analysis

-

Cost-based reconstruction estimates

-

Consideration of regulatory or statutory constraints

6. Case Illustration: Hypothetical Portfolio Valuation

A multinational corporation owns a 50,000 m² mixed-use portfolio comprising offices, retail space, and an industrial facility.

-

Step 1: Segregate property types

-

Step 2: Apply income capitalization for retail and industrial units, adjusting for vacancy and operating expenses

-

Step 3: Use DCF for office building with variable lease income

-

Step 4: Cross-validate using cost approach for specialized assets

-

Step 5: Compile portfolio valuation for consolidated reporting under IFRS

Outcome: Provides an auditable, standards-compliant valuation with sensitivity analysis to account for market fluctuations, lease renewal risks, and ESG compliance costs.

7. Challenges in Corporate Valuation

-

Market Volatility: Interest rates, macroeconomic cycles, and geopolitical risks affect value.

-

Data Limitations: Emerging markets or thin transactional evidence require professional judgment.

-

Complex Ownership & Lease Structures: Multi-tenant arrangements, easements, and shared ownership complicate analysis.

-

Sustainability & ESG Factors: Energy performance, carbon compliance, and green building certifications increasingly influence valuations.

8. Technology and Innovation

Emerging technologies enhance accuracy, transparency, and efficiency:

-

Geographic Information Systems (GIS): Spatial analysis for location-specific risk assessment

-

PropTech platforms: Automated data aggregation, market analytics, and benchmarking

-

Advanced Financial Models: AI-enabled DCF and scenario analysis

-

Digital Reporting Tools: Interactive dashboards, audit-ready documentation

Technology complements professional judgment, enabling real-time market insights and faster, more defensible valuations.

9. Implications for Corporate Strategy

Corporate valuation supports:

-

Investment Decisions: Acquisition, disposition, and development strategy

-

Portfolio Optimization: Rationalization and capital allocation

-

Risk Management: Insurance, financing, and regulatory compliance

-

Governance: Board reporting, audit, and internal controls

High-quality valuation services ensure strategic alignment between real estate holdings and organizational objectives, enhancing decision-making, accountability, and transparency.

10. Conclusion

Corporate real estate valuation is a cornerstone of effective asset management, financial reporting, and strategic planning. Through methodical application of income capitalization, DCF, cost, and sales comparison approaches, corporate valuations provide credible, transparent, and defensible assessments. Compliance with IVS, RICS, and IFRS standards ensures consistency, professional integrity, and audit readiness. Emerging trends, including ESG integration, technological innovation, and post-pandemic real estate dynamics, highlight the evolving complexity of corporate valuation. Organizations leveraging rigorous valuation frameworks are better positioned to mitigate risk, optimize portfolios, and make strategic decisions that maximize value over the long term.

References / Suggested Readings

-

RICS (2022). RICS Valuation – Global Standards (Red Book). London: Royal Institution of Chartered Surveyors.

-

IVSC (2023). International Valuation Standards. London: International Valuation Standards Council.

-

Geltner, D., Miller, N., Clayton, J., & Eichholtz, P. (2014). Commercial Real Estate Analysis and Investments (3rd ed.). Cengage Learning.

-

Fanning, R. (2021). Corporate Real Estate and Strategic Asset Management. Journal of Property Investment & Finance, 39(5), 401–416.

-

IFRS Foundation (2023). International Financial Reporting Standards. London: IFRS Foundation.

Our Fact Checking Process

We prioritize accuracy and integrity in our content. Here's how we maintain high standards:

- Expert Review: All articles are reviewed by subject matter experts.

- Source Validation: Information is backed by credible, up-to-date sources.

- Transparency: We clearly cite references and disclose potential conflicts.

Your trust is important. Learn more about our Fact Checking process and editorial policy.

Our Review Board

Our content is carefully reviewed by experienced professionals to ensure accuracy and relevance.

- Qualified Experts: Each article is assessed by specialists with field-specific knowledge.

- Up-to-date Insights: We incorporate the latest research, trends, and standards.

- Commitment to Quality: Reviewers ensure clarity, correctness, and completeness.

Look for the expert-reviewed label to read content you can trust.

Join The Discussion